#5 Casper Sleep: Sleeping Its Way Through Losses

Bad unit economics: Declining revenue growth, mounting losses with no clear path towards profitability.

Highly competitive market: Crowded space, price-sensitive customers, and non-recurring revenue.

Misleading narrative around being a technology company.

IPO debacle and poor public market performance.

Business Overview

Casper is a public e-commerce company selling sleep products online and through retail stores. Their product offerings include mattresses, pillows, bed frames, sheets, and other sleep-related items.

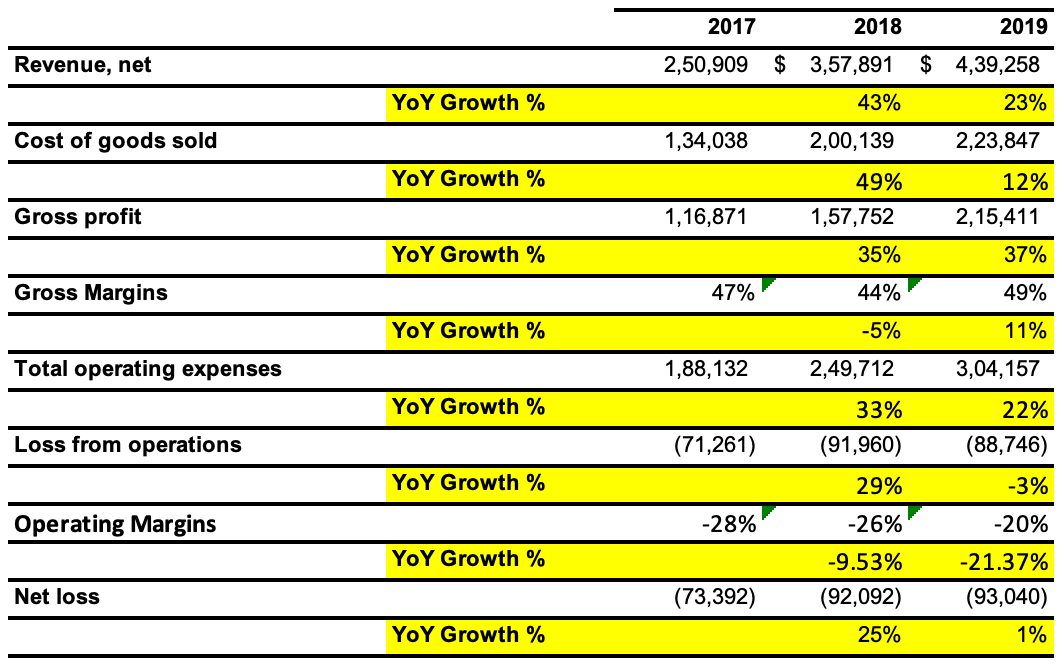

Financial Performance

Let's look at its core financial metrics:

Revenue: Revenue growth has been driven primarily by increased sales and marketing expenses since its inception. These numbers won't last, considering their bad results and decreased ability to raise capital at low costs.

Losses: The company has negative operating margins averaging -24% since 2017 and essentially lost the entirety of its Series D funding just in the year 2019.

Sales Efficiency: The company seems to be doing poorly as its efficiency was 1 in 2019(Created $1 in revenue for every dollar invested in sales and marketing). The only problem is that this revenue is non-recurring and the company lost $0.20 cents on every dollar of revenue, which makes the unit economics look unfavorable.

Debt: The company has $15.9 million of short-term debt and $50.0 million of long-term debt as of December 31, 2019. These are not awfully high numbers, but I wonder how the company manages to make these debt payments considering their bad unit economics.

There seems to be no clear path towards profitability considering the company has low margins, non-recurring revenue, declining revenue growth rate(even after raising large amounts of capital), and increasing losses. The company has made huge promises of getting better margins by controlling manufacturing in turn vertically integrating(another Silicon Valley buzz word). Honestly, I have no clue how the company plans to do this considering their poor results, high burn rate, mounting losses, and barely any cash on their balance sheet. I believe the company will eventually raise money through junk bonds and trade close to its 52 week low unless they pull off a miracle(Which I never discount being a true believer in outliers).

Confusion: Misleading technology narrative

Since its inception, Casper has created a narrative of being a technology company in the sleep space. This is fairly apparent as in its S-1, it talks about "As a pioneer of the Sleep Economy, we bring the benefits of cutting-edge technology, data, and insights directly to consumers." The company's valuation till now seems to have been driven by its flamboyant vision, which is valued in the private markets but without solid financial performance is punished in the public markets. In my opinion, this is the fundamental flaw in the company's history. Casper is just an e-commerce company that specializes in selling sleep products. The company utilizes technology to distribute its products, but there is no proprietary technology used to manufacture the products or analyze data around them.

Highly competitive market

The mattresses and sleep products industry is very price sensitive and faces intense competition. The space is large considering that every individual owns a mattress, but it's highly fragmented, almost no repeat customers(Individuals buy mattresses after years), and its discretionary nature makes it a difficult business. Casper does not have a competitive advantage because its product is not highly differentiated and often costs more than a normal mattress. This is a considerably bad time for Casper, considering that overall incomes are down, which directly correlates to the amount individuals spend on non-essential products.

IPO Debacle & Valuation

Just before its IPO in early 2020, Casper raised $100 M at a $1.1 B post-money valuation from renowned investors from across the world. But on the day of the IPO, the company's stock started trading at $12, pricing the company at a valuation of $490 M(This is even prior to the pandemic due to which the company's valuation hit its 52 week low of $127 M). Currently, the company is trading at a valuation of $370 M, which is almost 65% below its previous private round.

This is a solid sign to showcase that public market investors are very skeptical about private market valuations in current times, considering the record amount raised in venture and growth capital. I believe that the popularization of the blitzscaling approach has led so many startups down the road of capital inefficiency.

I believe that Casper is fundamentally a DTC mattress company that should stick to its core and try to build the company around the sleep economy. Any step to create huge changes will result in a capital structure change that will probably lead the company into bankruptcy. Key lessons for founders:

Chase product milestones/customer satisfaction and not valuation upgrades as metrics of success.

Think long term, create a competitive moat and seek lucrative unit economics.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.